Go paper-free

Amend paper-free preferences for your statements and communications.

Whether you’re buying your first home, moving on, or already with us, we’ll make every step as easy and stress-free as we can – so you can put your feet up and focus on feeling at home.

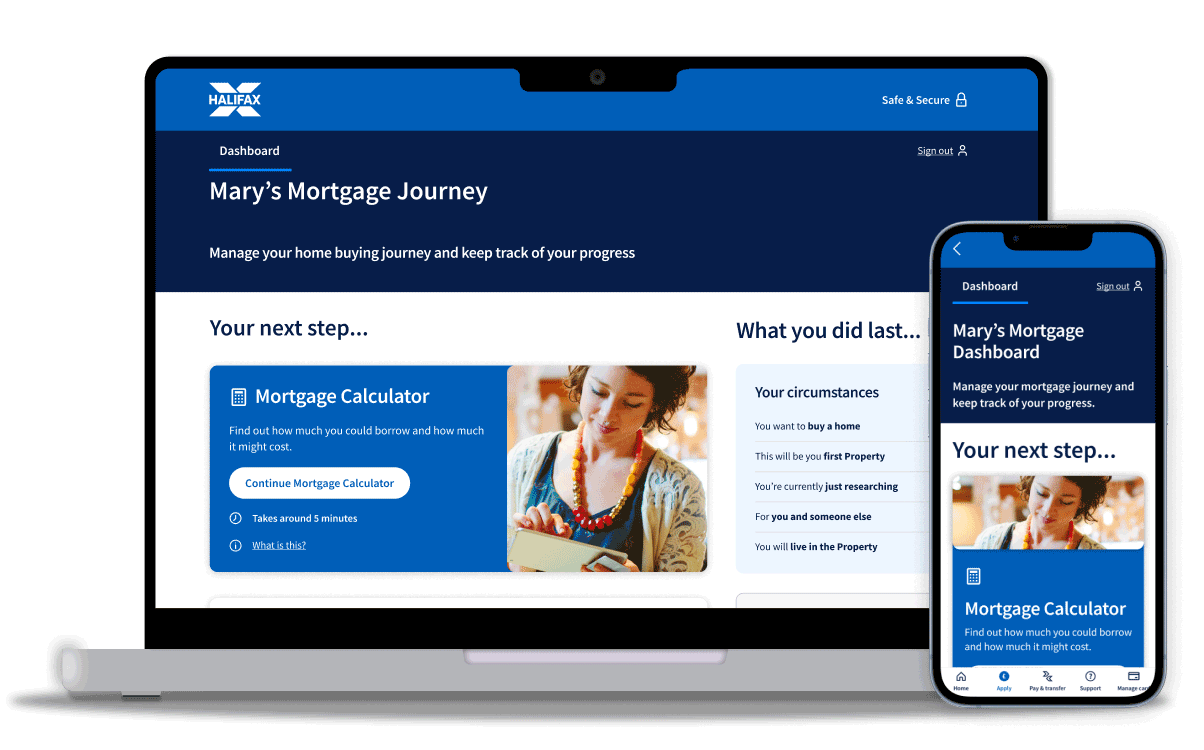

We make your mortgage journey simple

Track and manage your mortgage application online with your own mortgage dashboard. Upload documents, pick valuation options and get support, all in one place.

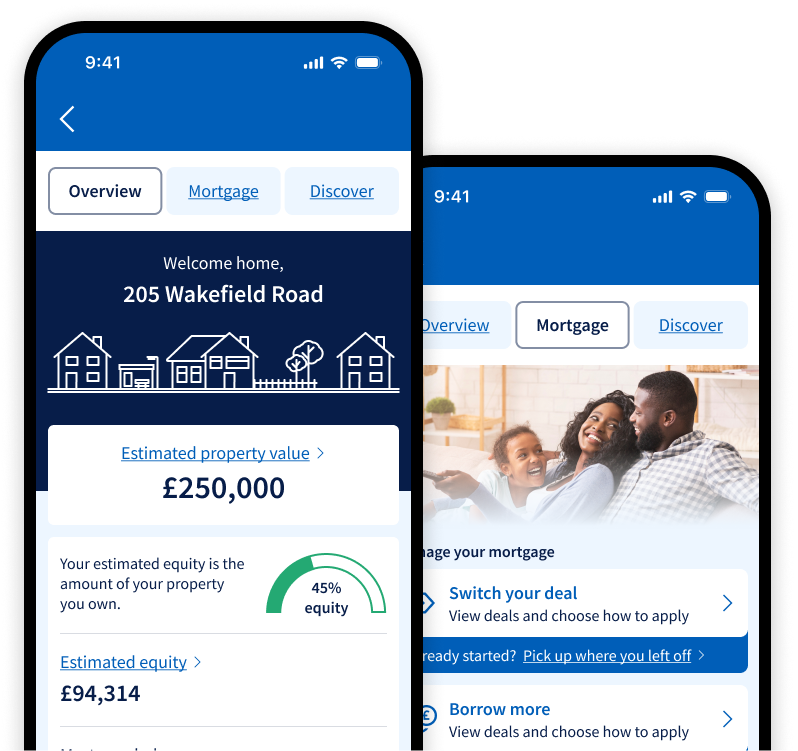

HelloHome on the Halifax app lets you track your rate and payments. Learn about your property value and equity. Even switch and save on household bills.

Conveyancing is the legal process for buying a home that’s done by a solicitor. Let Halifax help you with this next step.

We want to make sure you know about our other help and guidance options. Here’s one that might suit you.

View the latest data on house price trends in the UK.

Our free online events are designed to help you achieve your homebuying goals.