Go paper-free

Amend paper-free preferences for your statements and communications.

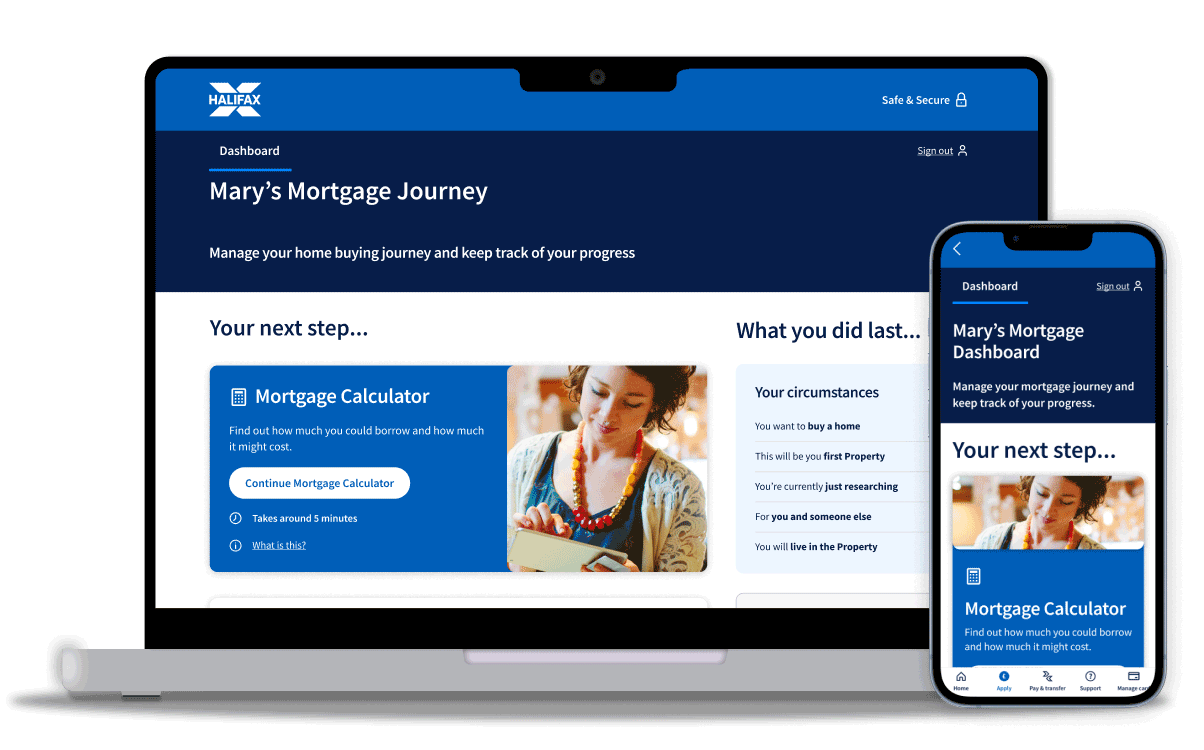

Buying your first home can be a big step. Our online mortgage calculator will give you a rough idea of how much you could borrow, and how much it could cost each month.

We make your mortgage journey simple

Track and manage your mortgage application online with your own mortgage dashboard. Upload documents, pick valuation options and get support, all in one place.

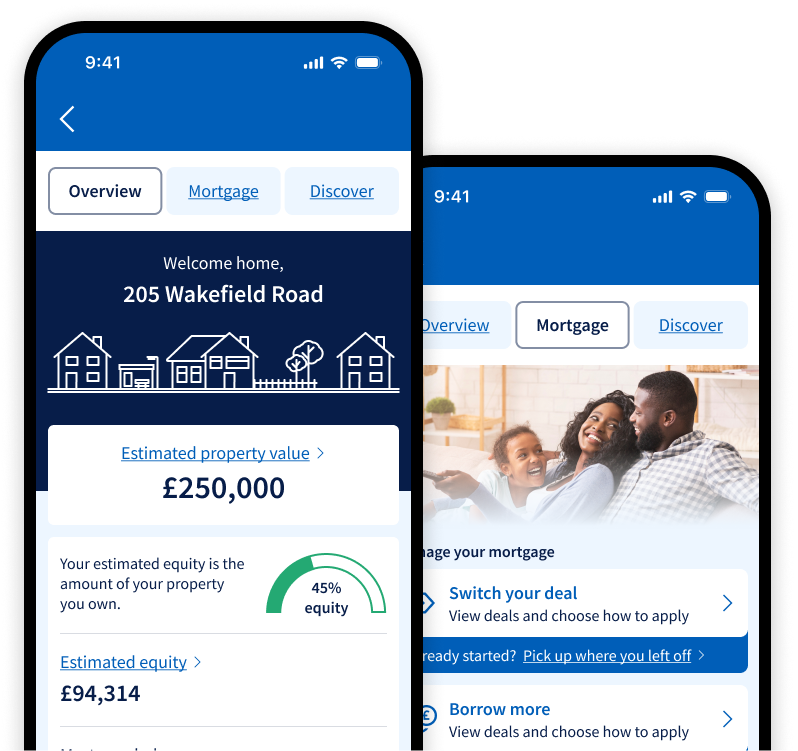

HelloHome on the Halifax app lets you track your rate and payments. Learn about your property value and equity. Even switch and save on household bills.

Learn about the process of buying your first home with our expert guides and resources. Get top tips on saving for a deposit, improving your credit score, making an application and more.

Explore our special offers to see if you could get more from your first home.

You may be able to apply online or speak to us over the phone

Before you start, make sure you’ve:

We want to make sure you know about our other help and guidance options. Here’s one that might suit you.