Go paper-free

Amend paper-free preferences for your statements and communications.

Running out of room? Thinking of downsizing?

Wherever your next move takes you, we’ve got the right mortgage for your plans.

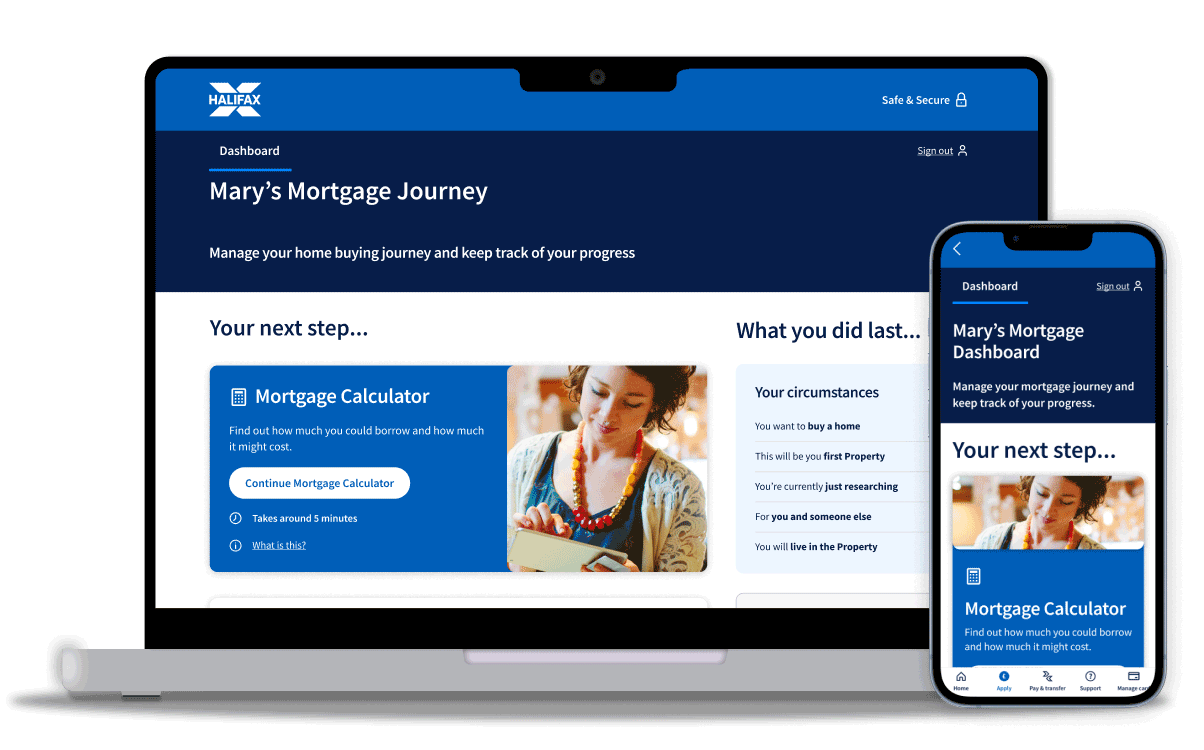

We make your mortgage journey simple

Track and manage your mortgage application online with your own mortgage dashboard. Upload documents, pick valuation options and get support, all in one place.

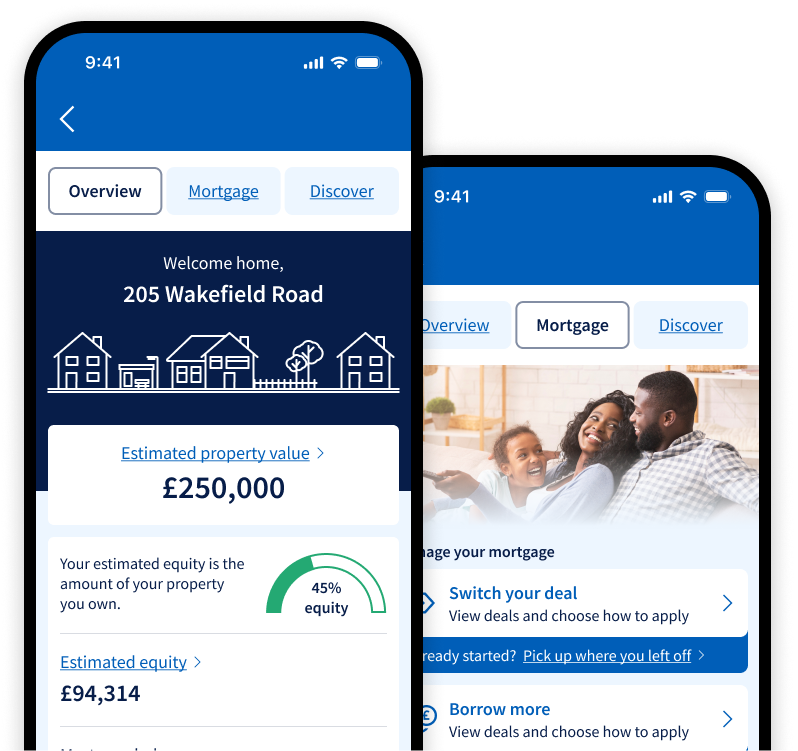

HelloHome on the Halifax app lets you track your rate and payments. Learn about your property value and equity. Even switch and save on household bills.

Take a look at our special offers. You may be able to apply for 1 or both.

When you’ve got your agreement in principle and found the perfect property, your next step is to complete a full mortgage application. You might be able to do this online, or you can speak to a mortgage and protection adviser.

Once you've completed your agreement in principle with us, we'll guide you through your online application. If you decide that you'd like some help, you can ask to speak to a mortgage and protection adviser at any point.

Already applying for a mortgage with us online?

Pick up where you left off using the log in details we gave you.

You can speak to us from the comfort of your sofa, either by phone or video.

When you're ready to take your next step, here are a few things you'll want to think about:

Applying online

You could continue your full mortgage application online. We'll guide you through your online application, step by step. And if you decide that you'd like some help, you can ask to speak to a mortgage and protection adviser at any point.

Speak to us

If you'd like some expert guidance with your application, our mortgage advisers are ready to help. You can choose to talk to us on the phone or by video call. If you'd rather talk to us in person, you can book an appointment at your nearest branch.

The average appointment time is 2 hours. If you’re applying with someone else, choose a date and time that suits you both.

To talk to us by video call or over the phone, call us.

Before you speak to us, it will help if you can get some documents and details together. This helps to save time and means we can spend more of your appointment trying to find the right deal for your needs.

Make sure you have the following ready:

Your mortgage adviser will:

We'll also arrange for the property to be valued. This is to make sure the property is worth the amount you've asked to borrow.

In Scotland, sellers must send us a Home Report including a survey, Energy Performance Certificate and Property Questionnaire.

When we've checked all your details and documents and are happy that everything is okay, we’ll send you a mortgage offer in the post.

You can keep up to date with the progress of your mortgage online using Your Mortgage Tracker.

Each time you use Your Mortgage Tracker, you'll need:

We’ve sent you a personalised link to the tracker in your confirmation email, or you can access Your Mortgage Tracker now.

You can access the Mortgage Tracker on Monday to Saturday from 6am to 10pm, and Sunday 6am to 9pm.

The legal side of buying and selling a property can be carried out by either a solicitor or licensed conveyancer. They’ll check who owns the property you want to buy, what’s included in the sale and whether there are any clauses in the property’s deeds you or your lender need to be aware of. In Scotland your solicitor will also put in your offer and negotiate for you.

You'll need to:

Who's involved:

You can use the Halifax Conveyancing Service to compare quotes from our approved panel of up to 200 conveyancing professionals. You can review the quotes and select a conveyancer based on what matters most to you - the price, the firm's service rating or their location.

Get a quote for your legal costs

Alternatively, you can appoint your own conveyancer. If you choose to use the Halifax Conveyancing Service, this can be arranged with you by your Halifax mortgage and protection adviser, during your mortgage appointment.

All conveyancers instructed through the Halifax Conveyancing Service offer a 'no completion, no legal fee' guarantee, so you'll have nothing to pay for the legal work done if the purchase falls through.

Although there will be no legal fees if the purchase falls through, if the conveyancer has made payments to third parties on your behalf, such as fees for searches, you'll need to make a payment to cover these charges.

On average, it takes around 2 to 3 months from appointing your conveyancer to exchanging contracts.

When you’ve read all the documents, your conveyancer will ask you if you’re happy to proceed with the purchase. They'll then ask you to sign the contract. When everyone is ready, contracts will be exchanged, usually by phone, to form a binding legal agreement to buy and sell.

Before exchanging contracts, you’ll need to:

Who’s involved:

Once you’ve exchanged contracts (or in Scotland when you've concluded missives) you can start to make your moving arrangements.

After you've exchanged contracts, your conveyancer will ask you to sign the mortgage deed. This is the official document needed to transfer your new home to your name. They'll also apply to us for the mortgage money and ask you for any balance they need to complete your purchase.

On the day fixed to complete the purchase, your conveyancer will send all the money needed to pay the balance of the purchase price to the seller’s conveyancer. They'll also call you to confirm when the legal process is complete. You’ll then be able to pick up the keys to your new home and move in.

We'll send a letter to your new address to tell you when the mortgage has started.

Once all the paperwork is complete and you've collected the keys, it’s a great time to make sure you’ve protected what matters.

Home insurance

You should already have buildings insurance as it is a requirement of your mortgage, but it’s also a good idea to take out contents insurance to protect your household goods and personal belongings.

Protecting your mortgage

You may also want to think about protecting your mortgage with our Life and Body Cover. This type of insurance can give you the peace of mind of knowing that your family will be able to keep your home, even if something happens to you. It could help to pay off your mortgage in the event of your death, or if you become too ill to work.

Our mortgage and protection advisers are on hand to discuss your situation and can help you to find the right options and level of cover for your needs.

You can find out more about protecting your mortgage, the cover we offer and how to get a personalised quote by visiting our Mortgage Protection page.

What you need to know

Our protection plans are provided by Scottish Widows, which, like us, is part of the Lloyds Banking Group. Scottish Widows protection products have no cash-in value at any time and cover will stop if you don’t pay your premiums. If the policy amount has not been paid out by the end of the selected term, the policy will end and you’ll get nothing back. You must be a UK resident aged between 18 and 59 to apply.

We'll only lend you a percentage of what the property is worth, so you'll need to put down some of your own money towards the cost of the property. We call this a deposit. Your deposit should be at least 5% of the property’s value. If you can put down more than 5%, you can often get a lower initial interest rate.

Lending is subject to an affordability assessment, credit score and a full mortgage application.

As well as your deposit, there are other costs associated with buying a property and taking out a mortgage. Typical ones that apply to most buyers include conveyancing fees, Stamp Duty Land Tax/Land and Buildings Transaction Tax (properties in Scotland), valuation fees and Land Registry fees. There are often unexpected costs too in buying a property, so it's a good idea to have a reserve fund to cover them.

Use our mortgage calculator to see how much you could borrow and what your monthly payments might be. Or, to get a better indication apply for an agreement in principle.

If you have a Halifax mortgage and you’ve decided you’d like to move home, you might be able to move your product with you. This is called 'porting‘. It could save you money by not having to pay early repayment charges. You’ll learn more about this in your appointment with a mortgage and protection adviser. Your illustration and offer letter will also say if any of your products are portable.

You can use our online calculator to get an idea of how much you could borrow. Or, to get a better indication you can apply for an agreement in principle, also know as a 'mortgage promise'. We'll start by asking about your income, for example your basic salary and any regular overtime or bonuses.

We'll also ask about your regular outgoings, for example credit card or personal loan repayments, and we'll take these off your income. After that, we make a further allowance for average day-to-day living expenses. This allows us to see how much we think you can afford for your mortgage payment each month. We accept US dollars, euros, Australian dollars, Indian rupees and Swiss francs when calculating your mortgage affordability.

As part of our process of assessing whether we think you can afford the loan, we'll ask your permission to contact a credit reference agency. They can give us information about:

We'll use credit scoring to help us decide whether to lend you money. Credit scoring works by awarding you points based on the information that:

We use this information to give you an indication of whether we'll lend you money as a mortgage and if so, how much.

An agreement in principle, also known as a 'decision in principle' or 'mortgage promise', is useful if you haven’t found a property you want to buy but would like to know how much you could borrow. All we need is a few personal details about you and anyone else who will be named on the mortgage. Then we’ll contact a credit reference agency for a credit search and give you a credit score. If you reach our pass mark, we’ll give you a certificate, so that you can show the seller you can get a loan.

An agreement in principle is subject to us performing further checks and so is not a guarantee that we'll be able to lend you the money, for this you need a mortgage offer.

A mortgage offer is issued by a lender once your mortgage application has been received and the necessary checks, such as the property valuation and confirmation of your details, have been carried out. It sets out the terms under which the lender is prepared to offer you a loan.

The property you buy must be located within the UK and loans can only be used to buy your main residential home or for purposes relating to this home.

We'll consider lending you money to buy different types of property. For some types of properties, we may ask you for a bigger deposit. Any loan we make will be subject to a satisfactory property valuation by a surveyor of our choice.

A mortgage has a key difference to other loans - it's secured against your home. If you can't keep up with your monthly repayments or you get into financial difficulties you should contact us straight away so we can give you the help you need.

House prices can rise or fall. If your home’s value becomes less than you owe, you’ll be in negative equity. If you need to sell and the sale price is less than your mortgage, you’ll face a shortfall you’ll need to repay.

Mortgages can last for a long time, so it's important that it's right for you. You'll need to think about such things as the type of loan, how long you want it for and what type of product you'd like.

Methods of repayment - there are 3 different ways of repaying your mortgage. These are repayment, interest-only, and a combination of repayment and interest-only.

Mortgage terms - Halifax mortgages can extend up to 40 years. The length of your mortgage affects your monthly payments and the overall cost. With a repayment mortgage, a longer term with lower monthly payments would take more time to repay. This would mean you'd pay more interest over time. As a result, the total cost of your mortgage would be higher.

With an interest-only mortgage, the length of the term makes no difference to the monthly payments because these are only paying off the interest charges and not the loan itself. With an interest-only mortgage your mortgage term needs to match the time when you'll have enough money in your repayment plan(s) to repay the loan.

Mortgage products - we may have different types of mortgage products with different types of interest rates. These change from time to time and we'll give you details of the current range when you apply.

Product incentives - from time to time we may offer mortgage products that include an incentive. Products with incentives may have slightly higher interest rates, so you need to consider whether the upfront benefit outweighs the lower rate you'd get without the incentive.

Your mortgage and protection adviser will ask you about your preferences and discuss your needs and circumstances before deciding which mortgage to recommend to you.

Return any requested documentation for your mortgage as soon as possible.

Work closely with your conveyancer to understand timings and next steps in the process – such as local authority search turnaround times.

Make sure all parties are working towards the same completion date and be aware of any chains you may be in which may impact this.

Consider any other third parties you’ll need to contact and get quotes from (for example, removal firms), and make sure they are aware of the completion date you are aiming for.

It's a requirement of your mortgage to have buildings insurance. This covers the bricks and mortar, fixtures and fittings. It's also a good idea to take out contents insurance as well - this protects all your possessions in your home, from furniture to jewellery.

It’s also important to think about what would happen to your mortgage in the event of your death, or if you are too ill to work. Our expert Mortgage and Protection Advisers can help you to find the right level of cover to protect your mortgage, should the worst happen.

This will depend on the mortgage product, there may be a product fee to pay and early repayment charges if you repay early. Any product fees can be added on to your mortgage on completion. There could be other charges and standard costs that you may have to pay during the course of setting up your mortgage. You'll be charged interest on any fees, charges and standard costs added to your loan.

There are other costs associated with buying a property and taking out a mortgage.

When you take out your mortgage, you arrange to have a fixed or variable rate product for a period of time. At the end of this time, the product will end and your loan will usually be transferred to a Lender Variable Rate. At this point, you may choose to move it to a new product for a further period of time.

We want to make sure you know about our other help and guidance options. Here’s one that might suit you.