Go paper-free

Amend paper-free preferences for your statements and communications.

Having your own business has many advantages. You’re able to call the shots, you don’t answer to anyone else, and you get to work on something you’re passionate about day in, day out.

All of these reasons are very powerful motivators to become the boss.

But what many people don’t see is that the life of an entrepreneur is far from glamorous. Small business owners work hard and have to cope with the pressure of always being on the job and the uncertainty that comes with owning your own business.

So why would you jeopardise all of this by not having the right insurance in place? The biggest reason business owners give for not investing in protection is that they're too small to need any insurance.

Sometimes the most important things come in small packages, and your business is no exception. Make sure you protect what's precious to you with public liability insurance.

Public liability insurance (also known as PL) isn’t just for big businesses. In fact, it’s important for small businesses too.

So, let’s start at the beginning. What is it? Well, the insurance provides cover if you're sued for damages by a member of the public (including clients) due to bodily injury or property damage suffered as a result of your work.

And this is why it’s so important because it safeguards against accidents happening. Even the most cautious of businesses can’t prevent accidents from happening entirely. That's because accidents, by nature, are unexpected and unintentional.

Take a look around you. The tools that you need to run your business can be a hazard if they’re put in unsuitable hands or left in the wrong place.

For this reason, the list of businesses that need public liability insurance is a long one. From plumbers and plasterers to carpenters and cake makers; there are very few professions and trades that don't require this type of insurance.

You should consider getting public liability insurance if:

Don’t fall into the trap of thinking that you don’t it just because you run a small business. Something as simple as a member of the public tripping over a ladder that you forgot to put away or spilling juice over a client's laptop, could cost you much more than your premium if you're uninsured.

The protection offered by public liability insurance covers a wide range of potential claims and, while you don’t have to have it by law, it will undoubtedly prove to be a valuable investment should the worst happen.

While public liability insurance is not a legal requirement for most businesses, it should be considered as an essential part of your toolbox, particularly if you interact with members of the public in any way.

Take the humble hammer as an example. If you dropped this heavy object while working in a clients’ home, you could cause damage that you’d be liable for. Even worse, if you left it lying around for a young child to pick up and they’re injured as a result, you could find yourself involved in an expensive and lengthy legal case. If this hasn’t convinced you that you need public liability insurance, then here are some more reasons to hammer the point home:

Public liability insurance is designed to cover damage to possessions, bodily injury, or death caused by your business for those persons not employed by you.

Having the cover in place will pay for successful compensation claims made by suppliers, clients or members of the public who feel that they have a case against you.

You’ll often hear public liability insurance referred to as cover for ‘slips, trips and falls’ and while this is true, there’s more to the insurance than just this.

Here are some examples of the types of claims that this insurance can cover you for:

Slips, trips and falls

If you’re working where there is heavy footfall from the public, your business is at risk of someone falling and hurting themselves as a result of yours or an employees' actions. It may seem like a small mishap at the time, but a small coffee spillage, an unattended tool or a loose cable can cause a hazard for those around you.

Accidents

Unfortunately, accidents can and do happen and are so unpredictable that they could occur at any time, anywhere to anyone. When you’re working with tools, in particular, accidents can be caused by merely dropping or misplacing them. Heavy tools can cause a lot of damage to your clients' property no matter how unintentional the act is.

Faulty work

Although this is a preventable type of claim, even the smallest of oversights can result in injury. If you have a business premises or clients come to your home, then it’s your responsibility to make sure that they’re fit for purpose. If an ill-fitted carpet results in a fall or a protruding screw head causes injury, then the consequences are as huge as any other incident.

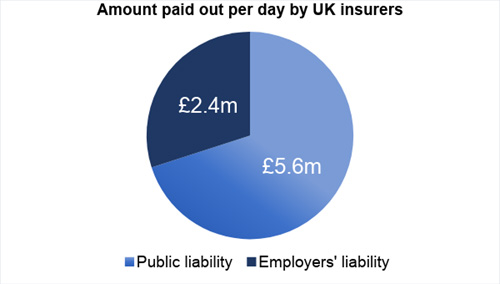

Note: Public liability insurance doesn’t cover injury to your employees or damage to their possessions. To protect those that work for you, you’ll need employers’ liability insurance which is a legal requirement for most businesses with staff.

Your business is unique, and the amount of public liability insurance you need could be different from someone else in the same profession or trade as you. It’s like asking ‘how long is a piece of string?’.

The answer to this question doesn’t relate to the size of your business though. Small businesses don't always need the minimum cover level, just as bigger enterprises may not need the most.

To help you understand how much risk your business is exposed to, regardless of its size, here are some things to consider:

How much contact does your company have with members of the public?

Depending on your business, you’ll have different interactions with the public. If you’re a cake maker, for example, a small number of clients may visit you every week to discuss designs and collect their cakes. In this case, you may decide that you only need the lowest standard of cover which is typically £1 million.

However, if you’re a hairdresser with a busy salon, your exposure increases dramatically. You may have clients and suppliers visiting your business premises all day, every day. For this type of business, you may conclude that £2 million is the right level of cover for you.

Do you have any contracts that require a certain level of public liability insurance?

It’s always best to check any contracts that you have, or are trying to win, to identify if a certain level of cover is required. Many local authorities will usually demand that you have a minimum cover level of £5 million before they’ll let you carry out any work.

Are any of your business activities excluded from the policy?

As with any insurance policy, public liability insurance will have exclusions that will not be covered in the event of a claim. Always give your insurance provider as many details as possible about your business and the work you do so that they can advise you on whether any exclusions may affect you.

Remember: Being underinsured is just as bad as having no insurance at all. Opting for the lowest level of cover in the hope that it will be cheaper could end up costing you more in the long run.

The most important thing is that you have the right amount of cover in place. The more information you’re able to provide the insurer about your business, the more accurate your cover and your premium will be.

Rather than viewing insurance as an unnecessary cost, see it as paying into your piggy bank so that if a claim needs to be made, your business isn’t left in financial ruin.

As a guide, the factors that influence your premium are:

This is one of the reasons that we work with Arthur J. Gallagher Insurance Brokers Limited, one of the UK’s largest Insurance brokers, who will source public liability quotes from a range of insurers. This allows you to select the quote that best suits your needs and your pocket

As with all insurance, it's essential that you weigh up the cost of your policy against the cost of a claim if you didn’t have insurance in place. You’ll generally find that paying an insurance premium is much cheaper than the cost of trying to sort things out yourself. After all, you can’t put a price on the peace of mind that insurance can give you and your clients.

If you’re looking for flexible public liability insurance to protect your business, then you can get a quick and easy online quote right now.

You’ll be able to tailor your cover to suit your needs and choose from a range of competitive quotes from a panel of leading insurers.

Within minutes you can get on with running your business knowing that if the unimaginable happened; you’re covered.