Go paper-free

Amend paper-free preferences for your statements and communications.

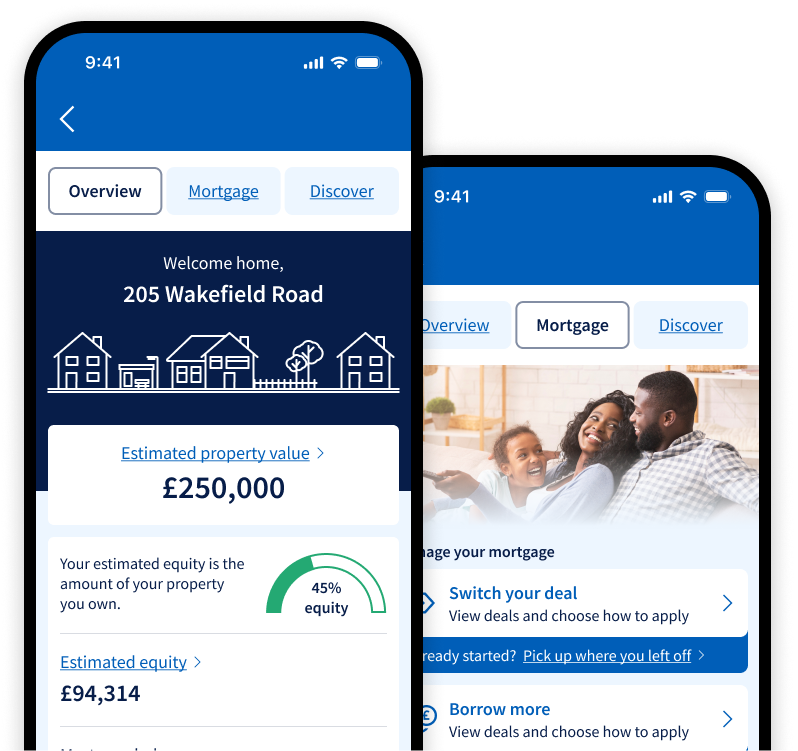

Find out what your mortgage rate might look like. Whether you’re a first time buyer or looking to switch, see how our mortgage interest rates compare.

HelloHome on the Halifax app lets you track your rate and payments. Learn about your property value and equity. Even switch and save on household bills.

Find out how to do more with your mortgage including switching to a new Halifax deal or borrowing more.

Your mortgage interest rate is the percentage of interest that you’ll pay on top of the money you borrow to buy a property. This varies from deal to deal, depending on several factors, such as:

There are a few different types of mortgage rate.

Mortgage interest rates are, essentially, how much it costs to borrow money from a lender to buy a property. The higher the interest rate, the higher your monthly mortgage payments are likely to be.

The type of mortgage you have will impact the amount of interest you pay. Fixed rate mortgages might come with a higher interest rate than a tracker mortgage, but there’s no guarantee your interest rate will stay the same with this type of variable mortgage.

With an interest only mortgage, your monthly payments only pay the interest earned on the amount you borrowed. You don’t pay back any of the loan itself. The full loan must then be paid back at the end of the term.

Mortgage interest rates can stay the same for years or they can change often. This depends on factors like the Bank of England base rate, the housing market and the state of the economy.

The type of rate can also have an impact. For example, a fixed rate mortgage has the same rate for however long your deal is.

If you’ve already applied for a Halifax mortgage, the rate we’ve offered you won’t be affected by any changes once the mortgage illustration has been accepted.

You should make sure you can afford to make your monthly payments, including interest. Consider the terms of the mortgage and the length of the product when and how much you’ll have to pay, and whether there are any fees involved.

If you’re considering a tracker mortgage, make sure you’ll be able to afford any increases to your repayments if the rate changes.